For our November/December expiration period, we now have 10 positions in play. Of the 10 positions, 7 out of 10 are now profitable, one is very close to profitability, one was not filled and one may require an adjustment--which we'll discuss later in the newsletter.

Progress Report--At this point we've got a 9% profit going for the month with a +90% probability of success.

That performance is excellent and we're on track for another good month--but perhaps the best thing about this style of trading is once the trade is established the market or the stocks we are trading on don't have to 'perform'--all that is necessary is the passage of time.

The odds are overwhelmingly in our favor--but there are always wild cards that can make things interesting. So with that in mind let's take a good look at...

The Market

The banking sector exploded higher this morning, along with the broader equity market, as Goldman Sachs added Citigroup Inc (C) to its "conviction list" and existing home sales climbed to a second consecutive month of gains--the National Association of Realtors reported existing home sales rose 10% to an annual rate of 4.53 million, up from a downwardly revised 4.12 million in August.

The bottom line is the uptrend is still intact.

This week, investors will see a number of earnings reports---177 S&P 500 companies are expected to report their quarterly performance, seven of which are listed on the Dow. Earnings are expected to be good; however, as we've seen in the last week any disappointment in either earnings or market outlook instantly triggers a sharp sell-off in that particular stock. With as much of a run as we've had it doesn't take much for investors to quickly lock in profits.

Even though there may individual stocks selling off the market will likely continue to rally--we’re coming to the beginning of the most bullish six months of the year. But the big driver is investors are counting on the Federal Reserve announcing additional measures to stimulate the economy. Known as "Quantitative Easing", the Fed is expected to unveil the new plan during their November 2-3 meeting.

The market appears to be in a holding pattern as investors turn their focus to another busy week of earnings reports, the U.S. mid-term elections and the Fed’s November 2-3 meeting.

Trader’s Tip:

Historically,

• October marks the end of the most bearish 6 month period for the Dow and S&P 500--as November heralds in the most bullish 6 months of the year. October also marks the end of the most bearish 4 months for the NASDAQ.

• October is known as the “bear killer”.

• October 28th is the 81st anniversary of the 1929 Crash where the Dow sank 23% in just two days.

• Thursday, October 28th and Friday, October 29th are historically bullish trading days.

Key Dates:

• November 18th--options expiration for some indices.

• November 19th--options expiration for all equity and all other index options.

What are the Secrets of the Week?

This week’s plays are both high-odds ETFs that give us plenty of room to be right---Our first play offers a +90% probability of success with an exceptional potential return of almost 12%. Our second play provides a +91% probability of win with a potential return on investment of 9%.

With such extreme complacency as shown in the volatility indices, it’s best to remain as neutral as possible until we get through 3rd quarter earnings, the U.S. mid-term elections and a conclusion as to what the Fed is really going to do. So let's get to it...

You can get in on this week's trades along with two new high-probability trades per week by clicking here now.

Stack the Deck on Every Trade,

Robert

Monday, October 25, 2010

NETFLIX (NLFX) JUMPED BY OVER TWENTY-DOLLARS AFTER ANNOUNCING BLOW-OUT EARNINGS WEDNESDAY NIGHT!

This past week the tug-o-war between earnings and economic news rocked the markets in both directions-- but our two new bullish plays spiked higher immediately after announcing...

NETFLIX (NLFX) JUMPED BY OVER TWENTY-DOLLARS AFTER ANNOUNCING BLOW-OUT EARNINGS WEDNESDAY NIGHT!

AND FREEPORT MCMORAN (FXC) SPIKED HIGHER BY OVER FOUR DOLLARS AFTER ANNOUNCING A TWENTY-SEVEN PERCENT PROFIT SURGE THURSDAY MORNING!

Those are some great earnings and stock performance---and we should be opening bottles of champagne and high-fiving each other--but both of these bullish plays were stopped out in the volatility immediately preceding their announcements! Now that hurts.

It's great to have been right on our analysis and direction of these two plays but the extreme choppiness of the markets early last week bounced us out before we could benefit from them. I know getting stopped out before the play takes off in our direction is super disappointing---but it's important to trade according to your discipline---especially with earnings plays. This one didn't turn out the way we wanted but we did play it the right way by setting solid safeguards to limit our losses--that's important and sticking to your discipline is something to be proud of.

The good news is earnings aren't over by a long shot and there are other stocks announcing with good prospects of moving the markets--and we're going to take advantage of that movement. To get an idea where the profits are this week let's take a good look at...

WHICH WAY THIS MARKET IS HEADED

The SP-500 rocked back and forth last week finishing up just seven points at 1183.08. That is not exactly a huge performance but it was another week of gains keeping the uptrend intact.

After spiking lower Tuesday morning the Nasdaq gained back all of its losses plus some to close at 2479--up 10.62 on the week. This index is still looking bullish and is continuing to move toward the yearly high at 2535.28---any move above that level would cause another round of short-covering.

However there is a lot of profit on the table---Amazon has rallied $65 since July---a 50% move--NetFlix is up 70% and AAPL is up 28% since August---and there are many others. With year-end for mutual funds coming up this Friday October 29 there are some good reasons to lock in gains.

However the big driver in this market is still intact--a Federal Reserve bent on flooding the market with more dollars. As long as those dollars are still flowing into stocks we could see some new highs before the end of the year--but not without some volatility along the way.

There were two economic reports for Friday and they both concerned employment-- Regional Employment and Mass Layoffs. The regional payroll report showed that 34 states lost jobs in September. with 23 states reporting a lower unemployment rate. However that lower unemployment rate can be deceiving because anyone running out of employment benefits fell off the rolls.

The Mass Layoff report showed the number of layoff events declined for the third consecutive month. They fell from 1,546 in August to 1,486 in September. The number of workers affected fell from 150,192 in August to 133,379 in September. Manufacturing still accounted for more than 25% of the layoffs. The slowing of layoffs suggests the economy is growing but still at a very slow pace.

Next week's economic calendar is active with multiple housing reports, Fed surveys and the GDP on Friday. The GDP will be the most important report for the week and our first look at the Q3 rate of growth. Estimates have risen slightly over the last month but the whisper numbers are still in the 1.6% range--pretty anemic but still positive.

Economic news is important but the real market mover is still earnings. So far over one third of the S&P has announced--out of the 158 S&P companies reporting 79.1% beat estimates, 7% reported inline and 13.9% missed. Those that beat estimates posted average gains in earnings of 47.4% while companies that missed averaged a -33.1% miss.

So far the SP-500 is showing reported earnings for the quarter increasing 26.21% over 2009Q3. That's some good performance but companies that are reporting inline are often getting sold hard after announcing--especially without a lot of positive forward guidance. Evidently expectations are pretty high and traders are selling quickly unless a company really outperforms-- a sign of weakening bullish sentiment.

This week we've got Microsoft reporting on Thursday after the close---the biggest tech stock to report this week. Also important are 3M, Texas Instruments, Merck and a ton of chip stocks.

Another big driver of this market is--and will continue to be--the value of the dollar. As the dollar declines stocks have been rising with commodity stocks is particular gaining ground as it takes more dollars to buy their output.

The value of the dollar hit center stage at the G-20 conference this weekend. Leading up to the conference on Thursday Timothy Geithner said that all the major currencies were roughly equal and then he circulated a letter to the other finance ministers on Friday telling them to hike the value of their currencies in order to increase the value of their exports on the U.S. market. As you can imagine that letter created a roar of protest.

The letter was seen as a direct attack on China and warned of the dangers of seeking "competitive advantage by either weakening their currency or preventing appreciation of undervalued currency." Those comments were seen as pretty hypocritical considering the U.S. is on a major quantitative easing program creating massive quantities of artificial money in order to lower interest rates and devalue the currency making U.S. exports cheaper. As you can imagine Geithner warning other countries about doing the same thing did not go over well at the meeting.

The Japanese Finance Minister called Geithner "unrealistic" and "difficult." He also warned "strong volatility in currency markets would be harmful to the stability of the global economy and financial system." The BRIC countries were united in their condemnation of the Geithner letter and said bluntly that the U.S. would not succeed in pressuring other countries to do what the U.S. was not doing itself.

Nothing was expected to result from the G20 meeting but the recent moves in currencies prompted traders to exercise caution and go flat over the weekend. When the meeting closed on Saturday there was "agreement" not to have a currency war--but ironically that is exactly what we've got.

One of the closing statements of the meeting by South Korean Finance Minister Yoon Jeung-Hyun showed exactly how much of the world sees the US today. He said the two-day G20 meeting had laid to rest fears of a currency war between "struggling debtors such as the United States" and "exporting powers such as China." Ouch--it seems the status of the US has fallen quite a bit in the last two years as the county is now being classified as 'a struggling debtor nation'.

So we've got a falling dollar, rising earnings and the promise of a conservative sweep in the November elections driving the markets higher--the question is whether those factors can keep powering the rally or are they already completely priced into the market?

The Fed's potential QE2 stimulus has been telegraphed for the last four weeks with almost daily speeches by Fed Governors touting the program. The S&P has gained 50 points since the September 21st FOMC statement. The market is convinced the Fed will act at ANY cost to insure economic growth. Analysts believe that $500 billion to $1 trillion of quantitative easing is now priced into the market but if it's anything less than that we could see some disappointed investors selling stocks.

Plus the market has priced in a Republican sweep on November 2nd but the closer we get to the election the tighter the races are becoming. The Democrats have a far larger budget than the Republicans. By some estimates the DNC and its offshoots have some $250 million to spread around in the last week of the campaign while the Republicans are closer to $100 million. With some of the hotly contested races attracting a blizzard of ads for the incumbents the odds of Republicans winning some of those seats are diminishing.

How this factors into the market on November 3rd is unknown. The groundswell of Republican support is shrinking but they are still expected to control the House. Will that be enough for businesses to breathe easier on hopes further government taxes and regulation will be postponed for at least two years? We won't know until after the smoke clears but a Republican victory is currently priced into the market and if anything else happens we could see a sell-off as well.

In spite of these potential pit-falls the big driver is still intact--the Fed's intention to create inflation by flooding the economy with cash. That force has been overcoming lesser fundamentals as wave after wave of cash finds a home in stocks. Bernanke wants to make it so painful to be in money markets and bond funds that people will eventually put the money into stocks--and that plan has been working--the question is...

HOW DO WE MAKE MONEY ON IT?

We've got two new plays lined up this week--one is bullish and the other bearish.

Our new bullish play is on a stock that looks ready to scream higher--the company just announced a new source of production that is TRIPLING their revenues. Plus what they produce increased in price as the dollar sinks. The stock has been climbing steadily since June but just retraced to its uptrend line giving us an extremely attractive entry point--one we'll be taking advantage of with some well-placed calls!

Our next play is just the opposite--the company announced decreasing sales over last year plus their forward guidance indicates even lower sales in the coming quarter and year. This company is struggling yet it's stock has climbed with the market to a new five month high and then rolled over this past week once earnings were known. This one looks ripe for some serious downside profit--an opportunity we'll be jumping on first thing Monday.

We've got two trades lined up to really move in their respective directions so let's get to it...

For more information on everything you receive with your Pearly Gates subscription click on www.cashflowheaven.com/pg

NETFLIX (NLFX) JUMPED BY OVER TWENTY-DOLLARS AFTER ANNOUNCING BLOW-OUT EARNINGS WEDNESDAY NIGHT!

AND FREEPORT MCMORAN (FXC) SPIKED HIGHER BY OVER FOUR DOLLARS AFTER ANNOUNCING A TWENTY-SEVEN PERCENT PROFIT SURGE THURSDAY MORNING!

Those are some great earnings and stock performance---and we should be opening bottles of champagne and high-fiving each other--but both of these bullish plays were stopped out in the volatility immediately preceding their announcements! Now that hurts.

It's great to have been right on our analysis and direction of these two plays but the extreme choppiness of the markets early last week bounced us out before we could benefit from them. I know getting stopped out before the play takes off in our direction is super disappointing---but it's important to trade according to your discipline---especially with earnings plays. This one didn't turn out the way we wanted but we did play it the right way by setting solid safeguards to limit our losses--that's important and sticking to your discipline is something to be proud of.

The good news is earnings aren't over by a long shot and there are other stocks announcing with good prospects of moving the markets--and we're going to take advantage of that movement. To get an idea where the profits are this week let's take a good look at...

WHICH WAY THIS MARKET IS HEADED

The SP-500 rocked back and forth last week finishing up just seven points at 1183.08. That is not exactly a huge performance but it was another week of gains keeping the uptrend intact.

After spiking lower Tuesday morning the Nasdaq gained back all of its losses plus some to close at 2479--up 10.62 on the week. This index is still looking bullish and is continuing to move toward the yearly high at 2535.28---any move above that level would cause another round of short-covering.

However there is a lot of profit on the table---Amazon has rallied $65 since July---a 50% move--NetFlix is up 70% and AAPL is up 28% since August---and there are many others. With year-end for mutual funds coming up this Friday October 29 there are some good reasons to lock in gains.

However the big driver in this market is still intact--a Federal Reserve bent on flooding the market with more dollars. As long as those dollars are still flowing into stocks we could see some new highs before the end of the year--but not without some volatility along the way.

There were two economic reports for Friday and they both concerned employment-- Regional Employment and Mass Layoffs. The regional payroll report showed that 34 states lost jobs in September. with 23 states reporting a lower unemployment rate. However that lower unemployment rate can be deceiving because anyone running out of employment benefits fell off the rolls.

The Mass Layoff report showed the number of layoff events declined for the third consecutive month. They fell from 1,546 in August to 1,486 in September. The number of workers affected fell from 150,192 in August to 133,379 in September. Manufacturing still accounted for more than 25% of the layoffs. The slowing of layoffs suggests the economy is growing but still at a very slow pace.

Next week's economic calendar is active with multiple housing reports, Fed surveys and the GDP on Friday. The GDP will be the most important report for the week and our first look at the Q3 rate of growth. Estimates have risen slightly over the last month but the whisper numbers are still in the 1.6% range--pretty anemic but still positive.

Economic news is important but the real market mover is still earnings. So far over one third of the S&P has announced--out of the 158 S&P companies reporting 79.1% beat estimates, 7% reported inline and 13.9% missed. Those that beat estimates posted average gains in earnings of 47.4% while companies that missed averaged a -33.1% miss.

So far the SP-500 is showing reported earnings for the quarter increasing 26.21% over 2009Q3. That's some good performance but companies that are reporting inline are often getting sold hard after announcing--especially without a lot of positive forward guidance. Evidently expectations are pretty high and traders are selling quickly unless a company really outperforms-- a sign of weakening bullish sentiment.

This week we've got Microsoft reporting on Thursday after the close---the biggest tech stock to report this week. Also important are 3M, Texas Instruments, Merck and a ton of chip stocks.

Another big driver of this market is--and will continue to be--the value of the dollar. As the dollar declines stocks have been rising with commodity stocks is particular gaining ground as it takes more dollars to buy their output.

The value of the dollar hit center stage at the G-20 conference this weekend. Leading up to the conference on Thursday Timothy Geithner said that all the major currencies were roughly equal and then he circulated a letter to the other finance ministers on Friday telling them to hike the value of their currencies in order to increase the value of their exports on the U.S. market. As you can imagine that letter created a roar of protest.

The letter was seen as a direct attack on China and warned of the dangers of seeking "competitive advantage by either weakening their currency or preventing appreciation of undervalued currency." Those comments were seen as pretty hypocritical considering the U.S. is on a major quantitative easing program creating massive quantities of artificial money in order to lower interest rates and devalue the currency making U.S. exports cheaper. As you can imagine Geithner warning other countries about doing the same thing did not go over well at the meeting.

The Japanese Finance Minister called Geithner "unrealistic" and "difficult." He also warned "strong volatility in currency markets would be harmful to the stability of the global economy and financial system." The BRIC countries were united in their condemnation of the Geithner letter and said bluntly that the U.S. would not succeed in pressuring other countries to do what the U.S. was not doing itself.

Nothing was expected to result from the G20 meeting but the recent moves in currencies prompted traders to exercise caution and go flat over the weekend. When the meeting closed on Saturday there was "agreement" not to have a currency war--but ironically that is exactly what we've got.

One of the closing statements of the meeting by South Korean Finance Minister Yoon Jeung-Hyun showed exactly how much of the world sees the US today. He said the two-day G20 meeting had laid to rest fears of a currency war between "struggling debtors such as the United States" and "exporting powers such as China." Ouch--it seems the status of the US has fallen quite a bit in the last two years as the county is now being classified as 'a struggling debtor nation'.

So we've got a falling dollar, rising earnings and the promise of a conservative sweep in the November elections driving the markets higher--the question is whether those factors can keep powering the rally or are they already completely priced into the market?

The Fed's potential QE2 stimulus has been telegraphed for the last four weeks with almost daily speeches by Fed Governors touting the program. The S&P has gained 50 points since the September 21st FOMC statement. The market is convinced the Fed will act at ANY cost to insure economic growth. Analysts believe that $500 billion to $1 trillion of quantitative easing is now priced into the market but if it's anything less than that we could see some disappointed investors selling stocks.

Plus the market has priced in a Republican sweep on November 2nd but the closer we get to the election the tighter the races are becoming. The Democrats have a far larger budget than the Republicans. By some estimates the DNC and its offshoots have some $250 million to spread around in the last week of the campaign while the Republicans are closer to $100 million. With some of the hotly contested races attracting a blizzard of ads for the incumbents the odds of Republicans winning some of those seats are diminishing.

How this factors into the market on November 3rd is unknown. The groundswell of Republican support is shrinking but they are still expected to control the House. Will that be enough for businesses to breathe easier on hopes further government taxes and regulation will be postponed for at least two years? We won't know until after the smoke clears but a Republican victory is currently priced into the market and if anything else happens we could see a sell-off as well.

In spite of these potential pit-falls the big driver is still intact--the Fed's intention to create inflation by flooding the economy with cash. That force has been overcoming lesser fundamentals as wave after wave of cash finds a home in stocks. Bernanke wants to make it so painful to be in money markets and bond funds that people will eventually put the money into stocks--and that plan has been working--the question is...

HOW DO WE MAKE MONEY ON IT?

We've got two new plays lined up this week--one is bullish and the other bearish.

Our new bullish play is on a stock that looks ready to scream higher--the company just announced a new source of production that is TRIPLING their revenues. Plus what they produce increased in price as the dollar sinks. The stock has been climbing steadily since June but just retraced to its uptrend line giving us an extremely attractive entry point--one we'll be taking advantage of with some well-placed calls!

Our next play is just the opposite--the company announced decreasing sales over last year plus their forward guidance indicates even lower sales in the coming quarter and year. This company is struggling yet it's stock has climbed with the market to a new five month high and then rolled over this past week once earnings were known. This one looks ripe for some serious downside profit--an opportunity we'll be jumping on first thing Monday.

We've got two trades lined up to really move in their respective directions so let's get to it...

For more information on everything you receive with your Pearly Gates subscription click on www.cashflowheaven.com/pg

Monday, October 18, 2010

LAS VEGAS SAND (LVS) SHOT PAST OUR TRAILING TRIGGER ON MONDAY AND THEN REVERSED BLASTING US OUT OF OUR NOV 38 CALLS AT A SWEET SAME-DAY THIRTY-PERCENT PROFIT!

This past week the markets rocked low enough and high enough to bounce us out of every trade we had...

LAS VEGAS SAND (LVS) SHOT PAST OUR TRAILING TRIGGER ON MONDAY AND THEN REVERSED BLASTING US OUT OF OUR NOV 38 CALLS AT A SWEET SAME-DAY THIRTY-PERCENT PROFIT!

THEN OUR DIREXION DAILY 3X BULL FINANCIAL (FAS) BEAR CALL SPREAD EXPIRED WORTHLESS FRIDAY FOR AN EXTREMELY SATISFYING FIFTY-PERCENT GAIN!

That was the good news--but the volatility of the past week also stopped us out of the QQQQ and SKX at losses. This has been a tough market to trade but fortunately we've had our share of gains to off-set the losses. The question now is whether earnings will continue to drive us higher or are we in for a nasty reversal? To help answer that question let's take a good look at...

WHICH WAY THIS MARKET IS HEADED

The major indices just keep on climbing--mostly on the back of some good earnings this past week out of Intel and Google. A total of 109 S&P-500 companies report this week along with 11 Dow components. Only 46 S&P companies have reported so far with 83% beating estimates and 9% missing their targets. Since 1994 an average of 62% normally beat but that has risen to 77% over the last four quarters due to easy comparisons in the prior year.

Earnings are now expected to increase +24.2% over Q3-2009---a slight improvement from the 23.6% estimate just a week ago.

The real leader in the markets last week as the Nasdaq---Google, Apple and Amazon powered a huge breakout with the index now poised for an assault on the year's highs. There is a good chance Apple will copy Google's performance with earnings on Monday keeping the move alive. The next heavyweight is on Thursday with Amazon announcing for another possible index jump higher.

Apple broke out to a new high on Friday with a $12 gain after Goldman gave them a new price target of $500. Apple will report earnings on Monday after the close and they are expected to beat estimates by a mile. This will be the first full quarter of sales for the iPhone 4 and it has been sold out all quarter with most sales backordered. Net income is expected to rise +130% to $3.83 billion. That equates to earnings per share of $4.09 on revenue of $18.9 billion.

IPad sales are expected to be 4.8 million units. The iPad was about the only tablet available in Q3 but that will change dramatically in Q4 as everyone else rushes to get products out for the holidays.

In spite of a stellar market last week the elephant in the room right now is the financial sector. On Friday S&P cut Bank America to a hold from a strong buy due to ongoing foreclosure woes. The problems stem from the major banks using robo-signers to sign tens of thousands of foreclosure documents without adequately researching each loan. These employees signed thousands of affidavits testifying to facts about the loans when they actually knew no details of the specific loan they were signing. They were just pushing paper as fast as they could in order to process foreclosures.

The use of this automatic signing process has prompted foreclosure halts by the major lenders until a review of the process can be completed. At least one state has already sued Ally Financial and expects to sue the other major banks. The allegations of fraud at "every level of the process" is prompting thousands of homeowner suits as well as suits from the investors who bought the packaged loans.

Plus earlier this week attorneys general from all 50 states launched a joint investigation into allegations that mortgage companies mishandled documents in foreclosing hundreds of thousands of homes. There were foreclosure proceedings on 930,437 properties in Q3 according to RealtyTrac. One in every 139 homes received a foreclosure notice in Q3 and a record 288,345 homes were actually seized by the banks.

Dick Bove, with Rochdale Securities, said the banks could lose up to $80 billion from the various suits and forced buybacks. The investors who bought the original loans may have a way to force the banks to buy back all the mortgage securities at face value if they can prove there was fraud at any point in the process. The Federal Home Loan Bank of Chicago sued the major lenders claiming they failed to disclose underwriting standards and had errors in their documentation. The bank is trying to recover more than $3.3 billion they paid for residential mortgage bank securities that went bad.

Banks were struggling to post decent profits before this mess and now they are faced with having to take charges for litigation expenses and potential settlements. If this progresses to the point of having to buy back previously packaged loans it could devastate the sector.

The halt in foreclosures as the mess is sorted out will also slow down the housing market even more as the nearly 300,000 homes slated for foreclosure in Q4 are pushed out into Q1 or even Q2.. Since more than a third of home sales are distressed this delay will be a serious blow to the housing industry.

It's been said in the past that the financial sector leads the markets--but as you can see from the charts above the markets are climbing--why? The most powerful influence on this market has been a flood of cheap dollars trying to find a home--and those dollars are finding that home in the stock market and in hard commodities.

Bernanke alluded to another quantitative easing program in his speech on Friday. As long as the Fed is applying downward pressure to rates and the dollar---the market will continue higher.

A few-cent drop in the dollar may not seem like much but when played using billion dollar trades in the derivatives market that is a big move. There are roughly $653 trillion in outstanding derivatives contracts and much of that is currency based. Traders are shorting the dollar, which produces cash they use to go long another currency, commodities or stocks. This is a very crowded trade but it is still gathering momentum---there are thousands of hedge funds and institutional investors still leveraging up these trades as each day passes. That is putting upward pressure on everything denominated in dollars including stocks.

So the bottom line is that even though there are some serious problems with the financials--and unemployment is still high--the markets continue to climb as the Fed induced ocean of money finds its way into the markets. This kind of unrestrained money production is creating a bubble in the bond market and possibly even the stock market--and it won't end well--but our concern is what to trade this week and...

HOW TO MAKE MONEY ON IT

We've got two trades lined up this week and they are both bullish--and they are both on stock market heavy weights due to release earnings--and both show charts that look ready to soar.

But as good as these two plays look we're not going to just throw our fate to the winds--we've got an intriguing hedging technique lined up to really cut your cost of entry--and your risk--while still leaving the door open for some huge upside!

So with earnings releases hitting the markets and the trend still climbing let's get started...

For more information on everything you receive with your Pearly Gates subscription click on www.cashflowheaven.com/pg

LAS VEGAS SAND (LVS) SHOT PAST OUR TRAILING TRIGGER ON MONDAY AND THEN REVERSED BLASTING US OUT OF OUR NOV 38 CALLS AT A SWEET SAME-DAY THIRTY-PERCENT PROFIT!

THEN OUR DIREXION DAILY 3X BULL FINANCIAL (FAS) BEAR CALL SPREAD EXPIRED WORTHLESS FRIDAY FOR AN EXTREMELY SATISFYING FIFTY-PERCENT GAIN!

That was the good news--but the volatility of the past week also stopped us out of the QQQQ and SKX at losses. This has been a tough market to trade but fortunately we've had our share of gains to off-set the losses. The question now is whether earnings will continue to drive us higher or are we in for a nasty reversal? To help answer that question let's take a good look at...

WHICH WAY THIS MARKET IS HEADED

The major indices just keep on climbing--mostly on the back of some good earnings this past week out of Intel and Google. A total of 109 S&P-500 companies report this week along with 11 Dow components. Only 46 S&P companies have reported so far with 83% beating estimates and 9% missing their targets. Since 1994 an average of 62% normally beat but that has risen to 77% over the last four quarters due to easy comparisons in the prior year.

Earnings are now expected to increase +24.2% over Q3-2009---a slight improvement from the 23.6% estimate just a week ago.

The real leader in the markets last week as the Nasdaq---Google, Apple and Amazon powered a huge breakout with the index now poised for an assault on the year's highs. There is a good chance Apple will copy Google's performance with earnings on Monday keeping the move alive. The next heavyweight is on Thursday with Amazon announcing for another possible index jump higher.

Apple broke out to a new high on Friday with a $12 gain after Goldman gave them a new price target of $500. Apple will report earnings on Monday after the close and they are expected to beat estimates by a mile. This will be the first full quarter of sales for the iPhone 4 and it has been sold out all quarter with most sales backordered. Net income is expected to rise +130% to $3.83 billion. That equates to earnings per share of $4.09 on revenue of $18.9 billion.

IPad sales are expected to be 4.8 million units. The iPad was about the only tablet available in Q3 but that will change dramatically in Q4 as everyone else rushes to get products out for the holidays.

In spite of a stellar market last week the elephant in the room right now is the financial sector. On Friday S&P cut Bank America to a hold from a strong buy due to ongoing foreclosure woes. The problems stem from the major banks using robo-signers to sign tens of thousands of foreclosure documents without adequately researching each loan. These employees signed thousands of affidavits testifying to facts about the loans when they actually knew no details of the specific loan they were signing. They were just pushing paper as fast as they could in order to process foreclosures.

The use of this automatic signing process has prompted foreclosure halts by the major lenders until a review of the process can be completed. At least one state has already sued Ally Financial and expects to sue the other major banks. The allegations of fraud at "every level of the process" is prompting thousands of homeowner suits as well as suits from the investors who bought the packaged loans.

Plus earlier this week attorneys general from all 50 states launched a joint investigation into allegations that mortgage companies mishandled documents in foreclosing hundreds of thousands of homes. There were foreclosure proceedings on 930,437 properties in Q3 according to RealtyTrac. One in every 139 homes received a foreclosure notice in Q3 and a record 288,345 homes were actually seized by the banks.

Dick Bove, with Rochdale Securities, said the banks could lose up to $80 billion from the various suits and forced buybacks. The investors who bought the original loans may have a way to force the banks to buy back all the mortgage securities at face value if they can prove there was fraud at any point in the process. The Federal Home Loan Bank of Chicago sued the major lenders claiming they failed to disclose underwriting standards and had errors in their documentation. The bank is trying to recover more than $3.3 billion they paid for residential mortgage bank securities that went bad.

Banks were struggling to post decent profits before this mess and now they are faced with having to take charges for litigation expenses and potential settlements. If this progresses to the point of having to buy back previously packaged loans it could devastate the sector.

The halt in foreclosures as the mess is sorted out will also slow down the housing market even more as the nearly 300,000 homes slated for foreclosure in Q4 are pushed out into Q1 or even Q2.. Since more than a third of home sales are distressed this delay will be a serious blow to the housing industry.

It's been said in the past that the financial sector leads the markets--but as you can see from the charts above the markets are climbing--why? The most powerful influence on this market has been a flood of cheap dollars trying to find a home--and those dollars are finding that home in the stock market and in hard commodities.

Bernanke alluded to another quantitative easing program in his speech on Friday. As long as the Fed is applying downward pressure to rates and the dollar---the market will continue higher.

A few-cent drop in the dollar may not seem like much but when played using billion dollar trades in the derivatives market that is a big move. There are roughly $653 trillion in outstanding derivatives contracts and much of that is currency based. Traders are shorting the dollar, which produces cash they use to go long another currency, commodities or stocks. This is a very crowded trade but it is still gathering momentum---there are thousands of hedge funds and institutional investors still leveraging up these trades as each day passes. That is putting upward pressure on everything denominated in dollars including stocks.

So the bottom line is that even though there are some serious problems with the financials--and unemployment is still high--the markets continue to climb as the Fed induced ocean of money finds its way into the markets. This kind of unrestrained money production is creating a bubble in the bond market and possibly even the stock market--and it won't end well--but our concern is what to trade this week and...

HOW TO MAKE MONEY ON IT

We've got two trades lined up this week and they are both bullish--and they are both on stock market heavy weights due to release earnings--and both show charts that look ready to soar.

But as good as these two plays look we're not going to just throw our fate to the winds--we've got an intriguing hedging technique lined up to really cut your cost of entry--and your risk--while still leaving the door open for some huge upside!

So with earnings releases hitting the markets and the trend still climbing let's get started...

For more information on everything you receive with your Pearly Gates subscription click on www.cashflowheaven.com/pg

Monday, October 11, 2010

Knock Down a 79% Annualized Return with an Over 90% Probability of Success!

Awhile back at the 'How to Know the Perfect Time to Exit a Spread' webinar we talked about when to close a spread early--in other words, when to "Take the Money and Run!" The conclusion from that webinar was that whenever a credit spread has less than $0.05 cents remaining, it's a smart idea to close the trade and bag your profits because you instantly remove any further risk. Your margin is freed up for another spread and you can relax knowing the profits from the spread you closed are in the bag.

As we approach October expiration, consider closing out of any plays that have earned the majority of their credit---from about Wednesday on the market makers typically widen their bid/ask spreads making exits less efficient so either Tuesday’s close or Wednesday’s open would be a great time to close trades early. And depending on your risk tolerance, you may also even consider closing them out a bit earlier.

Of course there’s always the “option” to ride trades all the way to expiration and avoid further commissions---if a spread is really out of the money they’ll typically expire worthless and you'll keep all the credit---a great position to be in!

There's a lot more details on these and other exit strategies inside the Package Buyers' area of the website--for those of you with The Winning Secret trading package, you can just log in, click on the Video Tutorials tab and select the webinar you'd like to watch. And if you don't have the package yet, you can add this valuable information to your trading library right here.

Trader’s Tip:

Historically,

• October marks the end of the most bearish 6 month period for the Dow and S&P 500. It also marks the end of the most bearish 4 months for the NASDAQ.

• On 10/10/2008, the Dow lost 18.2%---1874 points---ending the week as the most bearish for the Dow in the history of Wall Street.

• October is known as the “bear killer”.

Key Dates:

• October 14th--options expiration for some indices.

• October 15th--options expiration for all equity and all other index options.

• November 18th--options expiration for some indices.

• November 19th--options expiration for all equity and all other index options.

Market Outlook

Friday, the Dow Jones industrial average closed above 11,000 for the first time in five months. Ironically, this 11K benchmark came the day before the three-year anniversary of the market's ALL-TIME high--and while investors remain hopeful that the Federal Reserve will take even more action to re-stimulate the economy, the Dow is still 22.3% below that remarkable day.

The release of a weak jobs report, along with a number of other bearish indicators---including the dollar losing more ground---has only fueled expectations that the Fed will announce a new program to encourage borrowing when it meets again after the mid-term elections. In addition to this new program, the traders are banking on the possibility that the Fed will print more dollars---another factor that sent the stock market rocketing higher last week.

This week, economic data will include consumer and producer prices, as well as retail sales and consumer sentiment. These reports should shed some light on whether or not the economy has slowed down enough to justify further action from the Fed.

Private employers, worried about potential tax hikes and the costs associated with health care, only added 64,000 workers last month which fell short of the 75,000 expected. Some 95,000 government jobs were axed which included temporary census employees. Overall, the unemployment rate is now holding steady at 9.6%.

While investors and traders wait to see if the Federal Reserve will take advantage of a window of opportunity, we’ll take this opportunity to take advantage of a 30-day window on a couple of ETF plays for the week...

What are the Secrets of the Week?

Our first play has been trading well within our short strikes since July--a perfect neutral candidate for a high-probability iron condor. And with one of the most bullish Septembers since the 1930’s now behind us, October is shaping up to be another strong month for the Bulls---what better time for a bull put spread?

Both plays are on ETFs and generate a generous 8-10% profit with an over 91% probability of success---and with only about a month’s time for these trades to play out, we definitely have the winds blowing in our direction. Let's get started...

You can get in on this week's trades along with two new high-probability trades per week by clicking here now. http://www.cashflowheaven.com/ws

Stack the Deck on Every Trade,

Robert

As we approach October expiration, consider closing out of any plays that have earned the majority of their credit---from about Wednesday on the market makers typically widen their bid/ask spreads making exits less efficient so either Tuesday’s close or Wednesday’s open would be a great time to close trades early. And depending on your risk tolerance, you may also even consider closing them out a bit earlier.

Of course there’s always the “option” to ride trades all the way to expiration and avoid further commissions---if a spread is really out of the money they’ll typically expire worthless and you'll keep all the credit---a great position to be in!

There's a lot more details on these and other exit strategies inside the Package Buyers' area of the website--for those of you with The Winning Secret trading package, you can just log in, click on the Video Tutorials tab and select the webinar you'd like to watch. And if you don't have the package yet, you can add this valuable information to your trading library right here.

Trader’s Tip:

Historically,

• October marks the end of the most bearish 6 month period for the Dow and S&P 500. It also marks the end of the most bearish 4 months for the NASDAQ.

• On 10/10/2008, the Dow lost 18.2%---1874 points---ending the week as the most bearish for the Dow in the history of Wall Street.

• October is known as the “bear killer”.

Key Dates:

• October 14th--options expiration for some indices.

• October 15th--options expiration for all equity and all other index options.

• November 18th--options expiration for some indices.

• November 19th--options expiration for all equity and all other index options.

Market Outlook

Friday, the Dow Jones industrial average closed above 11,000 for the first time in five months. Ironically, this 11K benchmark came the day before the three-year anniversary of the market's ALL-TIME high--and while investors remain hopeful that the Federal Reserve will take even more action to re-stimulate the economy, the Dow is still 22.3% below that remarkable day.

The release of a weak jobs report, along with a number of other bearish indicators---including the dollar losing more ground---has only fueled expectations that the Fed will announce a new program to encourage borrowing when it meets again after the mid-term elections. In addition to this new program, the traders are banking on the possibility that the Fed will print more dollars---another factor that sent the stock market rocketing higher last week.

This week, economic data will include consumer and producer prices, as well as retail sales and consumer sentiment. These reports should shed some light on whether or not the economy has slowed down enough to justify further action from the Fed.

Private employers, worried about potential tax hikes and the costs associated with health care, only added 64,000 workers last month which fell short of the 75,000 expected. Some 95,000 government jobs were axed which included temporary census employees. Overall, the unemployment rate is now holding steady at 9.6%.

While investors and traders wait to see if the Federal Reserve will take advantage of a window of opportunity, we’ll take this opportunity to take advantage of a 30-day window on a couple of ETF plays for the week...

What are the Secrets of the Week?

Our first play has been trading well within our short strikes since July--a perfect neutral candidate for a high-probability iron condor. And with one of the most bullish Septembers since the 1930’s now behind us, October is shaping up to be another strong month for the Bulls---what better time for a bull put spread?

Both plays are on ETFs and generate a generous 8-10% profit with an over 91% probability of success---and with only about a month’s time for these trades to play out, we definitely have the winds blowing in our direction. Let's get started...

You can get in on this week's trades along with two new high-probability trades per week by clicking here now. http://www.cashflowheaven.com/ws

Stack the Deck on Every Trade,

Robert

THE USO SHOT HIGHER MONDAY THEN REVERSED STOPPING US OUT OF OUR 34 CALLS AT AN EYE-POPPING TWO-HUNDRED-NINETY-SIX PERCENT PROFIT!

After a dip on Monday the markets blasted higher for the rest of the week--taking our USO play with along for the ride...

THE USO SHOT HIGHER MONDAY THEN REVERSED STOPPING US OUT OF OUR 34 CALLS AT AN EYE-POPPING TWO-HUNDRED-NINETY-SIX PERCENT PROFIT!

WE ALSO BAGGED A SMALL GAIN ON OUR YUM! BRANDS (YUM) STRADDLE AS THE STOCK TOOK OFF AFTER EARNINGS!

That was a good week. YUM could have been even better as the stock continued to the upside in the days following earnings--but we followed our discipline and were stopped out early--and fortunately at a profit. We also got out of STEC early at a loss as it wasn't performing---only to see the thing launch through the roof the day after our exit! Now THAT is a great example of why the markets can be frustrating!

The bottom line though is it was a VERY profitable week--and we've got two news trades lined up to continue the momentum--so let's get started by taking a good look at...

WHICH WAY THIS MARKET IS HEADED

The SP-500 closed at 1165 on Friday which are highs not seen since May. No matter what the news is this market just keeps steadily marching higher. There is an impressive 35% of the S&P 500 stocks trading at or near new 52-week highs and there were 41 S&P stocks that made new highs on Friday alone.

And all that bullishness is in spite of the fact that the Non Farm Payrolls report Friday was horrible and this earnings season is not shaping up to be all that great either. S&P earnings are expected to only increase from 8% to 10% while revenues are set to increase by only 2%--not exactly overwhelming numbers.

The Nasdaq closed at 2401 on Friday at highs also not seen since May and very close to the high of the day--another bullish signal. A move higher on Monday will force the shorts to cover continuing this rally. Apple broke its downtrend last week and is now threatening to make a new all-time high--another positive factor influencing the Nasdaq.

The only potential spoiler for the techs is the chip sector where we've seen a slew of chip warnings lately. Another company warned Thursday night and their shares fell -10% in trading on Friday. Kulicke & Soffa (KLIC) warned that revenue for the current quarter would be "significantly below" Q3 due to softening industry conditions. The company designs semiconductor assembly equipment and is sometimes seen as one of the strong bellwethers in the chip sector. A slowdown in KLIC business means a future slowdown in the chip sector in general. This makes Intel's earnings on Tuesday even more critical for the tech sector.

The focus this week will shift to Q3 earnings as Intel, JP Morgan, Google and GE headline the earnings calendar. Intel on Tuesday will be critical since the chip sector has been receiving almost daily downgrades due to lower than projected PC sales. If Intel lowers guidance again on Wednesday it could be a bad day for investor sentiment.

One testament to the bullishness of the markets right now is how bad the Non Farm Payrolls report was on Friday--and yet the indices continued to climb. The Non Farm Payrolls showed a headline loss of -95,000 jobs when almost everyone was expecting a gain. This was the largest loss of jobs in three months and July and August were revised lower by a total of 15,000 jobs. The preliminary benchmark revision for the prior 12-month period was an additional loss of -366,000 jobs!

The government was the biggest drag on employment last month with 159,000 job losses compared with a +64,000 gain in private payrolls. Private job creation declined slightly in Q3 to +274,000 from +353,000 in Q2. That trend is heading in the wrong direction. Federal payrolls declined -76,000 while state and local governments cut 83,000 jobs.

The unemployment rate was unchanged at 9.6% but the U6 unemployment rose to 17.1%---the highest since last December. The U6 number includes those without jobs and those who are working part time to pay the bills while searching for a job in their field. Instead of employment improving it is still getting worse. Those out of work for more than six months were 41.7% of the total while those out of work for less than a month rose to 19.1%---and again that trend is moving in the wrong direction.

And the thing is--the situation is actually worse that what is shown. What wasn't reported in these employment numbers are the 250,000 workers in 37 states that lost their jobs on October 2nd. Those jobs were part of the $5 billion in stimulus for the Temporary Assistance for Needy Families program. Tens of thousands of these workers lost their jobs when the program ended on October 1st. The exact count is unknown because each of the 37 states configured the programs differently but many states told the workers not to show up for work beginning on October 2nd. These layoffs were not included in the September payroll report because the program conveniently ended a couple days after the survey period for the last jobs report before the elections. The TANF was only one of the stimulus programs ending on October 2nd. Also ending was a $2 billion subsidized childcare program and a $2.1 billion boost for Head Start. Jobs will be lost from both of those programs as well.

So with an employment report that bearish--why did the markets go up on Friday?

Because traders believe the weak jobs report assures the Fed will initiate a new round of quantitative easing. That policy would continue to push the dollar lower and stocks higher. In their best "don't fight the Fed" style traders bought the dip and the market kept on climbing.

The Fed of course is trying to keep a lid on all this enthusiasm. Early Friday morning St Louis Fed President James Bullard tryed to dampen expectations when he said "policymakers could wait until December if they felt the need for greater clarity on the economic outlook." Also, "this upcoming FOMC meeting is going to be a tough call, because the economy has slowed but it hasn't slowed so much that it's an obvious case to do something." However he also said, "It does not seem like inflation is going to hit our target unless we take further action."

Dallas Fed President Richard Fisher cautioned about assuming the Fed would enact QE2. "The markets have drawn too quick a conclusion that this is a likely event. If it is to occur it will only occur after thoughtful discussion." He also warned that it is not clear if the benefits of further quantitative easing outweigh the costs.

But of course traders aren't buying this jaw-boning because they figure the Fed doesn't have a choice. The markets have clearly priced in a move at the November 3rd FOMC meeting but Fed heads are going out of their way to caution against considering it a done deal. This growing wave of caution could weigh on the markets if anyone actually begins to take it seriously.

Economic fundamentals are clearly weak and NOT heading in a positive direction but as we've seen that flat out doesn't matter--as long as the SP-500 stays above horizontal support at 1150 this market is likely moving higher. As long as the dollar is declining we should see stocks rise---assuming traders can get past Intel's report on Tuesday. It's unlikely the Fed will do anything to sabotage the markets before the elections so as long as corporate forward outlooks are reasonable stocks should keep driving higher--the question is...

HOW DO WE MAKE MONEY ON IT?

We've got two plays this week that look so gosh darn bullish it's enough to make me buy their actual stocks for my retirement accounts--but since buying stocks is against our religion here at The Pearly Gates--we're going to get into some high-odds calls instead!

Our first play is on a company that just increased sales to an all time high--right in the middle of the recession! They have a product that folks are jumping on left and right and the stock just jumped off of major support and is now heading decidedly higher--a move we'll be jumping on with some well-placed calls first thing Monday morning!

Our next play is on a company that just catapulted their revenue an astounding 51% equating to a half a billion dollars as money floods into the company from their overseas operations. This company is selling a product in Asia that is going like gang-busters--and their revenue shows it--and so does the trend of this incredible climber. We'll be jumping on board first thing Monday for what looks like another stellar ride to the upside!

We've got two excellent plays lined up on a market that wants to move so let's get to it...

For more information on everything you receive with your Pearly Gates subscription click on www.cashflowheaven.com/pg

THE USO SHOT HIGHER MONDAY THEN REVERSED STOPPING US OUT OF OUR 34 CALLS AT AN EYE-POPPING TWO-HUNDRED-NINETY-SIX PERCENT PROFIT!

WE ALSO BAGGED A SMALL GAIN ON OUR YUM! BRANDS (YUM) STRADDLE AS THE STOCK TOOK OFF AFTER EARNINGS!

That was a good week. YUM could have been even better as the stock continued to the upside in the days following earnings--but we followed our discipline and were stopped out early--and fortunately at a profit. We also got out of STEC early at a loss as it wasn't performing---only to see the thing launch through the roof the day after our exit! Now THAT is a great example of why the markets can be frustrating!

The bottom line though is it was a VERY profitable week--and we've got two news trades lined up to continue the momentum--so let's get started by taking a good look at...

WHICH WAY THIS MARKET IS HEADED

The SP-500 closed at 1165 on Friday which are highs not seen since May. No matter what the news is this market just keeps steadily marching higher. There is an impressive 35% of the S&P 500 stocks trading at or near new 52-week highs and there were 41 S&P stocks that made new highs on Friday alone.

And all that bullishness is in spite of the fact that the Non Farm Payrolls report Friday was horrible and this earnings season is not shaping up to be all that great either. S&P earnings are expected to only increase from 8% to 10% while revenues are set to increase by only 2%--not exactly overwhelming numbers.

The Nasdaq closed at 2401 on Friday at highs also not seen since May and very close to the high of the day--another bullish signal. A move higher on Monday will force the shorts to cover continuing this rally. Apple broke its downtrend last week and is now threatening to make a new all-time high--another positive factor influencing the Nasdaq.

The only potential spoiler for the techs is the chip sector where we've seen a slew of chip warnings lately. Another company warned Thursday night and their shares fell -10% in trading on Friday. Kulicke & Soffa (KLIC) warned that revenue for the current quarter would be "significantly below" Q3 due to softening industry conditions. The company designs semiconductor assembly equipment and is sometimes seen as one of the strong bellwethers in the chip sector. A slowdown in KLIC business means a future slowdown in the chip sector in general. This makes Intel's earnings on Tuesday even more critical for the tech sector.

The focus this week will shift to Q3 earnings as Intel, JP Morgan, Google and GE headline the earnings calendar. Intel on Tuesday will be critical since the chip sector has been receiving almost daily downgrades due to lower than projected PC sales. If Intel lowers guidance again on Wednesday it could be a bad day for investor sentiment.

One testament to the bullishness of the markets right now is how bad the Non Farm Payrolls report was on Friday--and yet the indices continued to climb. The Non Farm Payrolls showed a headline loss of -95,000 jobs when almost everyone was expecting a gain. This was the largest loss of jobs in three months and July and August were revised lower by a total of 15,000 jobs. The preliminary benchmark revision for the prior 12-month period was an additional loss of -366,000 jobs!

The government was the biggest drag on employment last month with 159,000 job losses compared with a +64,000 gain in private payrolls. Private job creation declined slightly in Q3 to +274,000 from +353,000 in Q2. That trend is heading in the wrong direction. Federal payrolls declined -76,000 while state and local governments cut 83,000 jobs.

The unemployment rate was unchanged at 9.6% but the U6 unemployment rose to 17.1%---the highest since last December. The U6 number includes those without jobs and those who are working part time to pay the bills while searching for a job in their field. Instead of employment improving it is still getting worse. Those out of work for more than six months were 41.7% of the total while those out of work for less than a month rose to 19.1%---and again that trend is moving in the wrong direction.

And the thing is--the situation is actually worse that what is shown. What wasn't reported in these employment numbers are the 250,000 workers in 37 states that lost their jobs on October 2nd. Those jobs were part of the $5 billion in stimulus for the Temporary Assistance for Needy Families program. Tens of thousands of these workers lost their jobs when the program ended on October 1st. The exact count is unknown because each of the 37 states configured the programs differently but many states told the workers not to show up for work beginning on October 2nd. These layoffs were not included in the September payroll report because the program conveniently ended a couple days after the survey period for the last jobs report before the elections. The TANF was only one of the stimulus programs ending on October 2nd. Also ending was a $2 billion subsidized childcare program and a $2.1 billion boost for Head Start. Jobs will be lost from both of those programs as well.

So with an employment report that bearish--why did the markets go up on Friday?

Because traders believe the weak jobs report assures the Fed will initiate a new round of quantitative easing. That policy would continue to push the dollar lower and stocks higher. In their best "don't fight the Fed" style traders bought the dip and the market kept on climbing.

The Fed of course is trying to keep a lid on all this enthusiasm. Early Friday morning St Louis Fed President James Bullard tryed to dampen expectations when he said "policymakers could wait until December if they felt the need for greater clarity on the economic outlook." Also, "this upcoming FOMC meeting is going to be a tough call, because the economy has slowed but it hasn't slowed so much that it's an obvious case to do something." However he also said, "It does not seem like inflation is going to hit our target unless we take further action."

Dallas Fed President Richard Fisher cautioned about assuming the Fed would enact QE2. "The markets have drawn too quick a conclusion that this is a likely event. If it is to occur it will only occur after thoughtful discussion." He also warned that it is not clear if the benefits of further quantitative easing outweigh the costs.

But of course traders aren't buying this jaw-boning because they figure the Fed doesn't have a choice. The markets have clearly priced in a move at the November 3rd FOMC meeting but Fed heads are going out of their way to caution against considering it a done deal. This growing wave of caution could weigh on the markets if anyone actually begins to take it seriously.

Economic fundamentals are clearly weak and NOT heading in a positive direction but as we've seen that flat out doesn't matter--as long as the SP-500 stays above horizontal support at 1150 this market is likely moving higher. As long as the dollar is declining we should see stocks rise---assuming traders can get past Intel's report on Tuesday. It's unlikely the Fed will do anything to sabotage the markets before the elections so as long as corporate forward outlooks are reasonable stocks should keep driving higher--the question is...

HOW DO WE MAKE MONEY ON IT?

We've got two plays this week that look so gosh darn bullish it's enough to make me buy their actual stocks for my retirement accounts--but since buying stocks is against our religion here at The Pearly Gates--we're going to get into some high-odds calls instead!

Our first play is on a company that just increased sales to an all time high--right in the middle of the recession! They have a product that folks are jumping on left and right and the stock just jumped off of major support and is now heading decidedly higher--a move we'll be jumping on with some well-placed calls first thing Monday morning!

Our next play is on a company that just catapulted their revenue an astounding 51% equating to a half a billion dollars as money floods into the company from their overseas operations. This company is selling a product in Asia that is going like gang-busters--and their revenue shows it--and so does the trend of this incredible climber. We'll be jumping on board first thing Monday for what looks like another stellar ride to the upside!

We've got two excellent plays lined up on a market that wants to move so let's get to it...

For more information on everything you receive with your Pearly Gates subscription click on www.cashflowheaven.com/pg

Thursday, October 7, 2010

How to Make Money with the Most Important Rule of Gap Trading

When you see a stock either gap or make a big move in a certain direction--and then flatten out--it doesn't mean the move is over by a long shot. In fact usually the stock is just resting up--waiting for the next jump. So here's the biggest key--always trade in the direction of the gap.

Here is a great example--on September 28th M&T Bank (MTB) was featured as the "short of the day" because it had gapped lower followed by a long red candle lower. Subscribers could have purchased the October $80.00 puts for just $.70--but as you can see the stock was flat for several days. But then yesterday the stock shot lower again launching those .70 cent puts to a whopping $4.20 turning a modest $700 into $4200--that's a stunning 500% profit in just 8 days!

This is the power of gap trading--this short came during a major market breakout to new highs and it demonstrates the incredible effectiveness of trading relative strength and weakness--exactly what the trades inside The Daily Report are based on. A new bullish trade and bearish trade is published inside the Options Success website every day and then a Live Update table shows what is really performing--making your trade selection easy. To take advantage of these kind of set-ups and get a Trading Package to put it all together click this link now.

Market Commentary - The market has broken out above major resistance at SPY 115 and it has been able to hold that level for two days. If it can tread water and get past tomorrow’s Unemployment Report, it will rally to the highs of the year in the next few weeks.

The economic news has been improving. Chicago PMI, ISM manufacturing, China’s PMI and ISM services all came in better than expected. This morning, initial jobless claims dropped 11,000 to a seasonally adjusted 445,000. That marks the fourth week of steady improvement. Retailers have been reporting strong numbers and 80% have posted sales gains. On average, retail sales rose 2.8% in September and that topped analysts’ estimates.

Tomorrow’s Unemployment Report is expected to show flat job growth. Private sector gains are projected to offset public sector job losses. If this actually transpires, the market will rally off of the number. Yesterday, ADP reported that the private sector lost 39,000 jobs when consensus estimates forecasted 18,000 new jobs. The market shrugged this news off. ADP has been lower than the government’s estimates for three straight months. If tomorrow’s Unemployment Report comes in better than -50,000 there is an excellent chance the market will move higher.

Initial jobless claims have been improving and the market will latch onto that silver lining. Economic numbers that would normally “disappoint” have been taken in stride. Asset Managers are anxious to buy stocks ahead of earnings season and the November elections. They have been waiting for a pullback but they never got one--now that the market has broken out above major resistance, they are scrambling to get long. No one wants to miss a year-end rally.

Earnings season officially kicked off this afternoon when Alcoa posted its numbers. Even though profits were down the company's outlook was good--and the stock is rising in the afterhours market. Basic metals have been improving and with Alcoa trading near the low end of its range the stock has room to run.

Banks don’t start announcing until later next week. This sector could post weak numbers, but that is already factored into the market. IPOs have been light, trading volumes are extremely low and financial reform will soon bite into profits. Semiconductors have lagged the market and they could be the catalyst for the next leg of this rally. The big releases will start the week of October 18th.

The economic and earnings news is light next week and that favors the bulls. The momentum is strong and if the market can survive tomorrow’s Unemployment Report, it has nothing standing in its way. The next two weeks should be bullish and so take profits on call positions as we approach the highs of the year. Most of the good news will already be “baked in” by the time November election results are posted.

China’s growth is intact and credit concerns in Europe have temporarily subsided. These are two potential spoilers for this rally but they shouldn't come into play for the remainder of this year. Stocks are cheap relative to bonds and money will flow from fixed income into equities. Any decline should be swift and shallow presenting a buying opportunity.

In spite of the market's bullishness there are long-term issues that make it difficult to be overly optimistic. As 2011 rolls around, unemployment, structural deficits and higher taxes will weigh on the market. For now, if the SPY is above 115 so stay long. To find out what is performing right now--and what is likely to--get inside the Daily Report by clicking right here: http://www.cashflowheaven.com/os.

Trade Well,

Pete

Here is a great example--on September 28th M&T Bank (MTB) was featured as the "short of the day" because it had gapped lower followed by a long red candle lower. Subscribers could have purchased the October $80.00 puts for just $.70--but as you can see the stock was flat for several days. But then yesterday the stock shot lower again launching those .70 cent puts to a whopping $4.20 turning a modest $700 into $4200--that's a stunning 500% profit in just 8 days!

This is the power of gap trading--this short came during a major market breakout to new highs and it demonstrates the incredible effectiveness of trading relative strength and weakness--exactly what the trades inside The Daily Report are based on. A new bullish trade and bearish trade is published inside the Options Success website every day and then a Live Update table shows what is really performing--making your trade selection easy. To take advantage of these kind of set-ups and get a Trading Package to put it all together click this link now.

Market Commentary - The market has broken out above major resistance at SPY 115 and it has been able to hold that level for two days. If it can tread water and get past tomorrow’s Unemployment Report, it will rally to the highs of the year in the next few weeks.

The economic news has been improving. Chicago PMI, ISM manufacturing, China’s PMI and ISM services all came in better than expected. This morning, initial jobless claims dropped 11,000 to a seasonally adjusted 445,000. That marks the fourth week of steady improvement. Retailers have been reporting strong numbers and 80% have posted sales gains. On average, retail sales rose 2.8% in September and that topped analysts’ estimates.

Tomorrow’s Unemployment Report is expected to show flat job growth. Private sector gains are projected to offset public sector job losses. If this actually transpires, the market will rally off of the number. Yesterday, ADP reported that the private sector lost 39,000 jobs when consensus estimates forecasted 18,000 new jobs. The market shrugged this news off. ADP has been lower than the government’s estimates for three straight months. If tomorrow’s Unemployment Report comes in better than -50,000 there is an excellent chance the market will move higher.

Initial jobless claims have been improving and the market will latch onto that silver lining. Economic numbers that would normally “disappoint” have been taken in stride. Asset Managers are anxious to buy stocks ahead of earnings season and the November elections. They have been waiting for a pullback but they never got one--now that the market has broken out above major resistance, they are scrambling to get long. No one wants to miss a year-end rally.

Earnings season officially kicked off this afternoon when Alcoa posted its numbers. Even though profits were down the company's outlook was good--and the stock is rising in the afterhours market. Basic metals have been improving and with Alcoa trading near the low end of its range the stock has room to run.

Banks don’t start announcing until later next week. This sector could post weak numbers, but that is already factored into the market. IPOs have been light, trading volumes are extremely low and financial reform will soon bite into profits. Semiconductors have lagged the market and they could be the catalyst for the next leg of this rally. The big releases will start the week of October 18th.

The economic and earnings news is light next week and that favors the bulls. The momentum is strong and if the market can survive tomorrow’s Unemployment Report, it has nothing standing in its way. The next two weeks should be bullish and so take profits on call positions as we approach the highs of the year. Most of the good news will already be “baked in” by the time November election results are posted.

China’s growth is intact and credit concerns in Europe have temporarily subsided. These are two potential spoilers for this rally but they shouldn't come into play for the remainder of this year. Stocks are cheap relative to bonds and money will flow from fixed income into equities. Any decline should be swift and shallow presenting a buying opportunity.

In spite of the market's bullishness there are long-term issues that make it difficult to be overly optimistic. As 2011 rolls around, unemployment, structural deficits and higher taxes will weigh on the market. For now, if the SPY is above 115 so stay long. To find out what is performing right now--and what is likely to--get inside the Daily Report by clicking right here: http://www.cashflowheaven.com/os.

Trade Well,

Pete

Monday, October 4, 2010

Knock Down a 68% Annualized Return with an Over 91% Probability of Success!

One of our subscribers---John---recently sent in an email with a question about limit orders---we’ve touched on this before during several of our webinars, but with many new subscribers onboard, it's time we reviewed the technique.

(If you are a Winning Secret package holder, you can log into the package buyers' area of the website to review any of the webinars--and if you're not, you can get your hands on one right here.)

John writes:

“I notice that when you enter a trade you don't get filled at the market. Do you use the margin spread to calculate a value higher than the market for the Sell to Open and a lower value for the Buy to Open? How do you determine these values?”

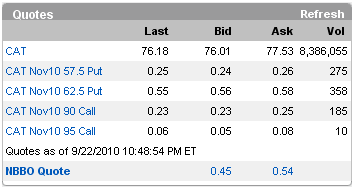

When placing an order, it can be beneficial to negotiate for a higher credit based on the bid, ask and spread amount. As an example, let's say we want to put on an Iron Condor for Caterpillar (CAT). If we look at the chart below, we can see the "NBBO (National Best Bid and Offer) Quote of $0.45 (Bid) by $0.54 (Ask)" with the difference between the two possible net credits---the bid/ask spread---being $0.54 - $0.45 = $0.09.

What most retail traders don't know is that this spread amount (the $0.09) is actually negotiable with the market makers---as a rule of thumb, about 30-40%. Generally, you can just divide the difference by a third ($0.09 / 3 = $0.03) and then add that amount back on to the bid price ($0.45 + $0.03 = $0.48). You can then set a limit price on the order form for $0.48. It may not seem like much but it makes a big difference over time as far as your return on investment.

Thanks for your question, John!

Trader’s Tip:

Historically,

• October marks the end of the most bearish 6 month period for the Dow and S&P 500. It also marks the end of the most bearish 4 months for the NASDAQ.

• On 10/10/2008, the Dow lost 18.2%---1874 points---ending the week as the most bearish for the Dow in the history of Wall Street.

• October is known as the “bear killer”.

• Tuesday, October 5th is a bearish trading day.

Key Dates:

• October 14th--options expiration for some indices.

• October 15th--options expiration for all equity and all other index options.

• November 18th--options expiration for some indices.

• November 19th--options expiration for all equity and all other index options.

Market Outlook

Last week the markets traded mostly flat after digesting the largest rise any September has seen since 1939. Even though consumer confidence dropped to its lowest level since February, traders are just more focused on encouraging signs in the corporate world including an increase in deal-making. Unfortunately, there's a big difference of opinion between Main Street and Wall Street on how the economy is doing. The focus, right now, is more on executives than consumers.

On Wednesday, European and U.S. markets fell as labor protests across the EU fueled worries about countries' ability to reduce their heavy debt. Demonstrations in Brussels, as well as Spain, Ireland and Portugal were observed as labor unions protested against problems and debt caused by the banks. The unrest has raised concerns that countries, such as Spain which may be downgraded again soon, will have difficulty repairing their public finances. Germany has pushed for tougher regulations while France is against near-automatic sanctions saying politicians and not unelected officials in Brussels should determine government policy.

However even wide-spread European unrest couldn't undermine the euro and boost the dollar--the dollar has fallen to a nine month low as the specter of more 'quantitative easing' (money printing) by the Fed drives the dollar lower and commodities higher.